At the beginning of the month, the average 30yr fixed rate was around 6%. Now it’s closer to 7%. That’s not a typo, but it may be a surprise considering the widespread media coverage of the Freddie Mac weekly rate survey, which reported a modest jump from 6.12 to 6.32 this week.

Freddie isn’t wrong, but the data is now stale. Due to its methodology, Freddie’s survey is essentially a measure of this past Monday’s rates versus the previous Monday, but not reported until Thursday. Thus, any additional movement throughout the week goes unreported until the following week.

In addition to being stale, the survey rate includes a certain amount of additional upfront closing costs (aka “points”). Understandably, it’s easy for those costs to get lost in the shuffle if we’re reading headlines like “mortgage rates rise to 6.32% this week.”

By the time we account for the additional upfront costs and the remaining days of the week (all of which saw additional increases in rates), the average lender is actually closer to 6.8% for a conventional 30yr fixed according to MND.

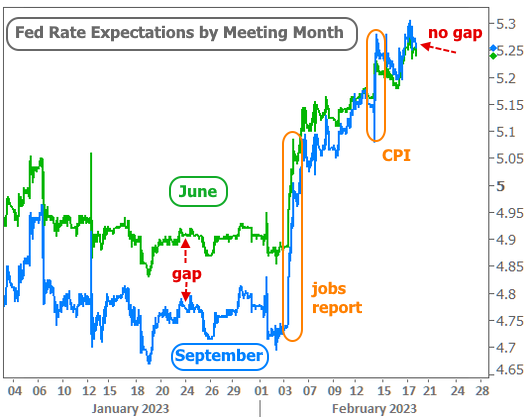

February’s abrupt rate spike has been driven by economic data. It began with the jobs report on February 3rd but continued with this week’s Consumer Price Index (CPI), the most impactful inflation report. Financial markets see this data having an impact on the Fed’s rate hike outlook.

Whereas the Fed was previously seen cutting rates as early as September, markets now expect the Fed to keep rates high through the end of the year. The Fed Funds Rate doesn’t directly dictate mortgage rates, but changes in the market’s outlook for the Fed’s rate tend to line up with mortgage rate momentum quite well. The following chart shows the September rate outlook rising in line with June’s rate outlook whereas traders had seen September’s rate being lower until early February.

Let’s take a closer look at this week’s key contributor to the upward pressure: CPI. The Fed would prefer the annual pace of inflation per CPI to be 2% at the “core” level (market jargon for an inflation number that excludes the more volatile food and energy prices). Core CPI is definitely not anywhere close to 2%.

OK, but it’s falling, right? And if it continues to fall, perhaps we can foresee a return to 2% in the future. Markets understand it will take time for annual numbers to fall. That’s why monthly numbers are more important these days. Unfortunately, the monthly numbers remained elevated in this week’s data.

The chart above shows some promise with monthly CPI certainly not as high as it had been. On the other hand, it ticked higher from last month and has yet to move below 0.3% for well over a year. Some simple math tells us a monthly reading of 0.3% would put annual inflation at 3.6%, which is still way too high for the Fed to consider cutting rates. If core CPI were to be operating in the 0.1-0.2 range for several months, mortgage rates would have a much easier time calming down and moving back into the 5% range.

Away from the inflation front, other economic data continues sending mixed signals. The second biggest report of the week ended up working against us. Retail Sales had been in negative territory for a few months, but surged up to +3.0% in January (reported this week).

The following day, a less consequential (but still important) report on inflation at the wholesale level–the Producer Price Index (PPI) painted a similar picture. Core PPI rose to 0.5% from 0.3% last month, far exceeding analyst expectations.

While inflation may indeed fall into line in the coming months, and while economic data may increasingly show the restrictive effects of higher interest rates, until those changes are more apparent in the data, rates will have a hard time moving too much lower.

The Fed’s approach to its rate-setting policy is also an important ingredient in the outlook. Several Fed members speculated that the pace of rate hikes could increase back to 0.50% per Fed meeting. That would be significant as the Fed just downshifted to 0.25% hikes at the last meeting and had been fairly unified in communicating that 0.25% would be the appropriate pace going forward.

We’ll hear a bit more from the Fed next week, but the catch is that it will be a historical account of the meeting that took place on February 1st. Markets will be interested to see how much debate there had been about downshifting to 0.25%. Traders will also tune in to various Fed speeches throughout the week to see if the next meeting is at risk of seeing a bigger rate hike.